Requirements to comply with Belgian regulations

Background

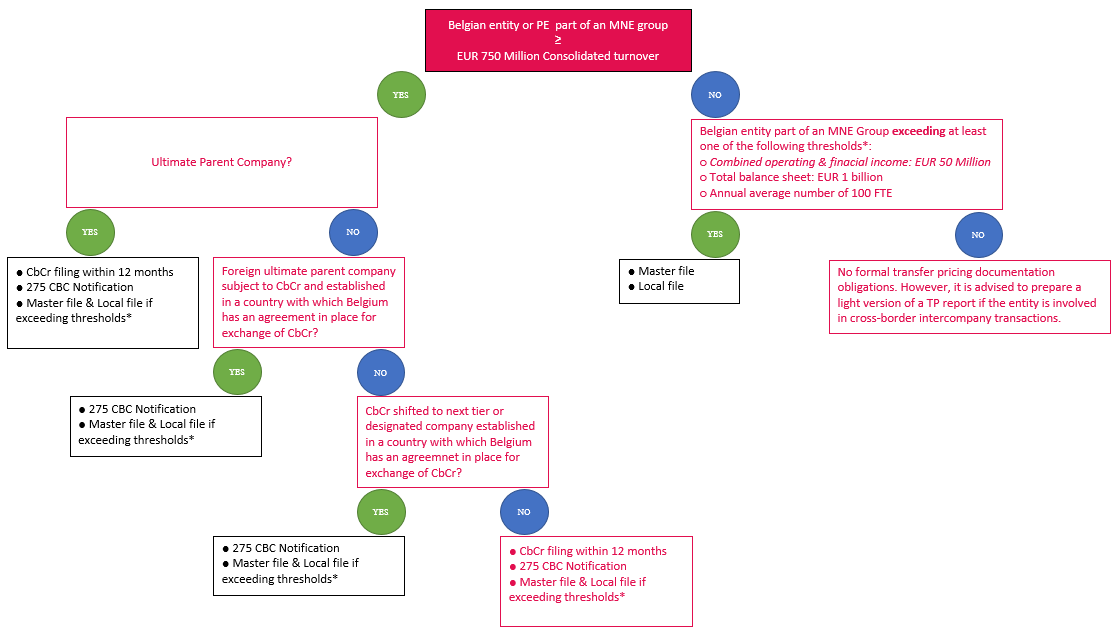

The Program act of 1 July 2016 introduced mandatory transfer pricing documentation requirements for certain multinationals. The reporting requirements have 3 objectives:

Three-tiered reporting

The documentation requirements consist of a three tiered reporting scheme:

Thresholds

Master file and Local file

Each Belgian company or permanent establishment (of a multinational group) that satisfies one of the below thresholds (to be assessed on the basis of the stand-alone financial statements of the Belgian entity of the preceding financial year) is obliged to file a “Master file” and a “Local file”:

In order to comply with the Belgian regulatory framework, the Belgian company that satisfies one of the above thresholds, is required to submit a Master file form (275 MF) and a Local file form (275 LF) for which more information follows below.

We note that the Local file Form is not the same as an OECD compliant Local File. Such OECD compliant Local File is however strongly recommended for those Belgian entities that are obliged to complete the Local file Form.

CbCr

Belgian legal entities, branches and taxable permanent establishments that are part of a multinational group with a consolidated gross revenue of EUR 750 million or more (or an equivalent in a foreign currency) (during the financial year preceding the financial year most recently closed) have to meet CbCr obligations, i.e. Country-by-Country notification (CbC notification or form 275 CBCNOT) or Country-by-Country Report (CbC report or form 275CBC) in case of the ultimate parent company or local filing.

Forms

The forms to comply with the documentation requirements have been published in the Belgian State Gazette of 2 December 2016:

Where to find the forms:

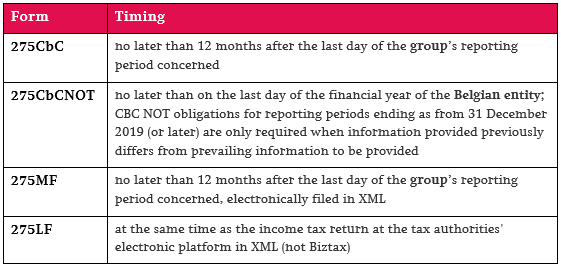

Format & Timing

Please note that these documents should be filed electronically in a valid XML format through the MYMINFINPRO platform. We can provide you with the Guidelines published by the Ministry of Finance and/or assist in filing these Forms.

Penalties

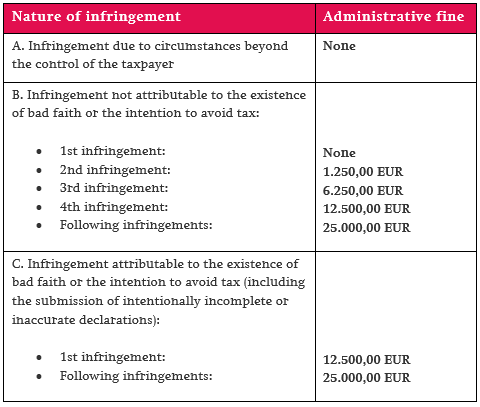

The Royal Decree implementing article 445, §3 of the Belgian Income Tax Code 1992 detailing the scale of the administrative penalties and their application rules applicable in the event of failure to comply with the transfer pricing obligations has been published in the Belgian Official Gazette on July, 9th 2018. The below table lists the nature of the infringements as well as the related administrative fines.

The following actions can amongst others be considered as infringements:

Our value proposition

TP documentation made easy. Click here

Your key contacts